Insolvency vs Bankruptcy: Basic Differences Explained

Bankruptcy and insolvency are complex words often mixed up or used interchangeably. However, bankruptcy and insolvency are two different things, and it is essential to understand the difference between them to make an informed decision.

A bankrupt individual is considered insolvent, but an insolvent individual isn’t equal to a bankrupt one. The terms also have multiple applications. For instance, bankruptcy typically refers to individuals and insolvency to businesses. Let’s have a closer look at both terms.

What Is Insolvency?

While bankruptcy and insolvency refer to excessive debts, being insolvent is a state leading to bankruptcy declaration if the situation doesn’t improve. Simply put, you are insolvent when you cannot repay the lenders.

While declaring bankruptcy is one solution to becoming insolvent, it doesn’t necessarily lead to it. You can change your insolvency status using other options based on your situation, like applying for a debt consolidation loan or making a consumer proposal.

There are two main types of insolvency:

Cash-Flow Insolvency

A company or individual enters cash-flow insolvency if their assets exceed their liabilities, but the liquid capital is insufficient to repay the debts. This means you own a property worth more than your debts but don’t have enough cash to repay the debt.

Such a situation can quickly be resolved with negotiation, where the creditors might agree to wait until your assets are sold to get their payment instead of taking legal action. We can help you with a Personal Insolvency Agreement or a Part 9 Debt Agreement with your creditors.

Balance-Sheet Insolvency

Balance sheet insolvency is when your outstanding debt is higher than the overall worth of your assets. Again, this insolvency is also not necessarily terminal, as individuals or companies might have enough cash flow to continue making repayments to their creditors. If you cannot do this, you might file for bankruptcy.

A business can’t become bankrupt. For a business, the process is insolvency or Liquidation, but they also have the options for Receivership and Voluntary administration if the company has a possibility of navigating through the difficult financial situation and becoming solvent again.

What Is Bankruptcy?

This proceeding offers relief and protection to individuals and sole traders who can’t repay their debts and have no means of doing so. When declaring bankruptcy, you will be assigned a licensed insolvency trustee responsible for liquidating all owned assets, investigating your financial situation, and contacting creditors.

You will be obliged to comply with the requests of your Trustee and need to share all your financial details with your Trustee. While you can still work or run a business, it has certain restrictions.

Bankruptcy in Australia lasts three years and one day, and your name would be included in public records. The AFSA will keep a permanent record of your bankruptcy with the Bankruptcy Inspector General. Anyone can access the bankruptcy records for a fee and view them on the National Personal Insolvency Index (NPII). In certain circumstances, your name can be hidden from this public record, and your name will be on the record for up to five years.

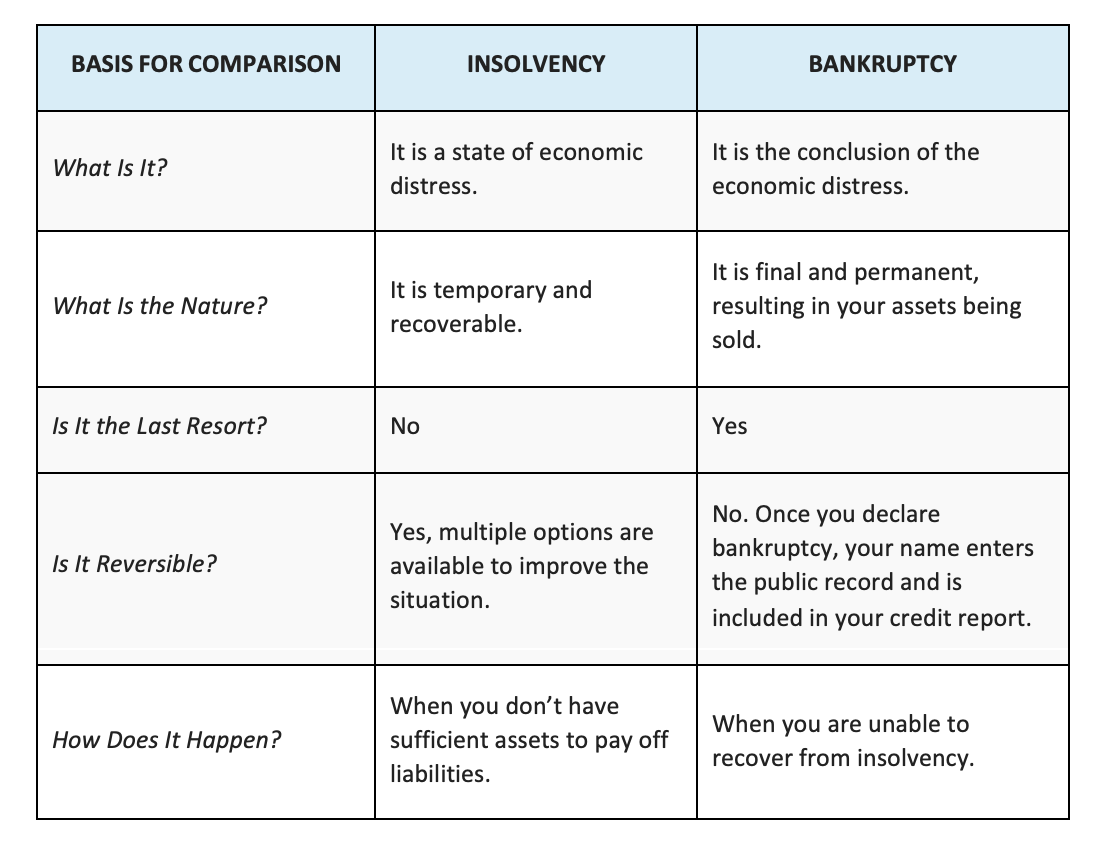

The Differences Between Insolvency and Bankruptcy Simplified

Here are some of the main differences between insolvency and bankruptcy for further understanding:

- Bankruptcy is a court order or a legal process, while insolvency is a distressed financial state.

- Bankruptcy is not the only resolution for insolvency.

- Bankruptcy applies to sole traders and individuals with restricted liability, while insolvency applies to businesses and individuals.

- Insolvency is a state of financial distress, while bankruptcy is the final resolution of insolvency that can’t be improved.

Here is a comparison chart:

Your Options with Insolvency vs Bankruptcy

Your Options with Insolvency vs Bankruptcy

Your Options with Insolvency vs Bankruptcy

Your Options with Insolvency vs BankruptcyBankruptcy should be your last resort, so it is essential to go over your options with insolvency and avoid bankruptcy. According to the Bankruptcy Act 1966, there are four main options for insolvency, and each comes with its own set of consequences:

- Temporary Debt Protection (TDP): When you apply for this option, you only get 21 days of protection from creditors’ pursuit. You would need professional assistance and advice during these days to develop the ideal action plan to improve your financial situation.

- Personal Insolvency Agreements: These agreements are made between you and all the creditors you owe to determine a payment plan to either pay the lump sum or pay in instalments at a specified period.

- Debt Agreements: These are binding agreements you make with your creditors to pay back the amount you can afford.

- Bankruptcy: If all else fails, you can file for bankruptcy. The typical bankruptcy in Australia lasts for three years and one day, and you would be released from most of your debts, but the bankruptcy will appear on your credit report for a few years, depending on your situation.

Insolvency vs Bankruptcy vs Liquidation

Liquidation is winding up and finalising an insolvent company’s financial affairs. Under usual circumstances, the Liquidation of company assets begins because the company cannot pay all its debts. In other words, it is insolvent. An independent and suitably qualified person, known as a liquidator, will take control of the company so that the business can wind up its affairs in an orderly and fair way for the benefit of all creditors.

Declaring Bankruptcy: When Is the Right Time?

Bankruptcy provides immense relief from your debts, but it shouldn’t be a decision taken lightly as it can significantly impact your life. Declaring bankruptcy means you might lose your assets, affecting your credit score for years.

You may not be able to apply for a mortgage or other forms of credit, and you can’t become a company director until you are released from bankruptcy. Moreover, it would be best to abide by certain obligations and restrictions during and after your bankruptcy.

We recommend that you consult with a bankruptcy expert as soon as possible to weigh up your options – by waiting too long, you may lose access to some of the alternatives to bankruptcy.

Bankruptcy vs Insolvency Australia

Bankruptcy and insolvency denote the lack of finances and the ability to pay your debts. However, unlike bankruptcy, insolvency is not the last resort, and you can improve your business or personal financial situation. If you have become insolvent or are on the brink of bankruptcy, you need professional advice immediately. It is a stressful time, and the proper guidance can improve your situation and prevent you from going bankrupt. There are multiple ways of dealing with insolvency based on your case to avoid bankruptcy.